Global Markets

Shein's Slowing Growth Threatens Hong Kong IPO Valuation

724FinanceKemal Tekin

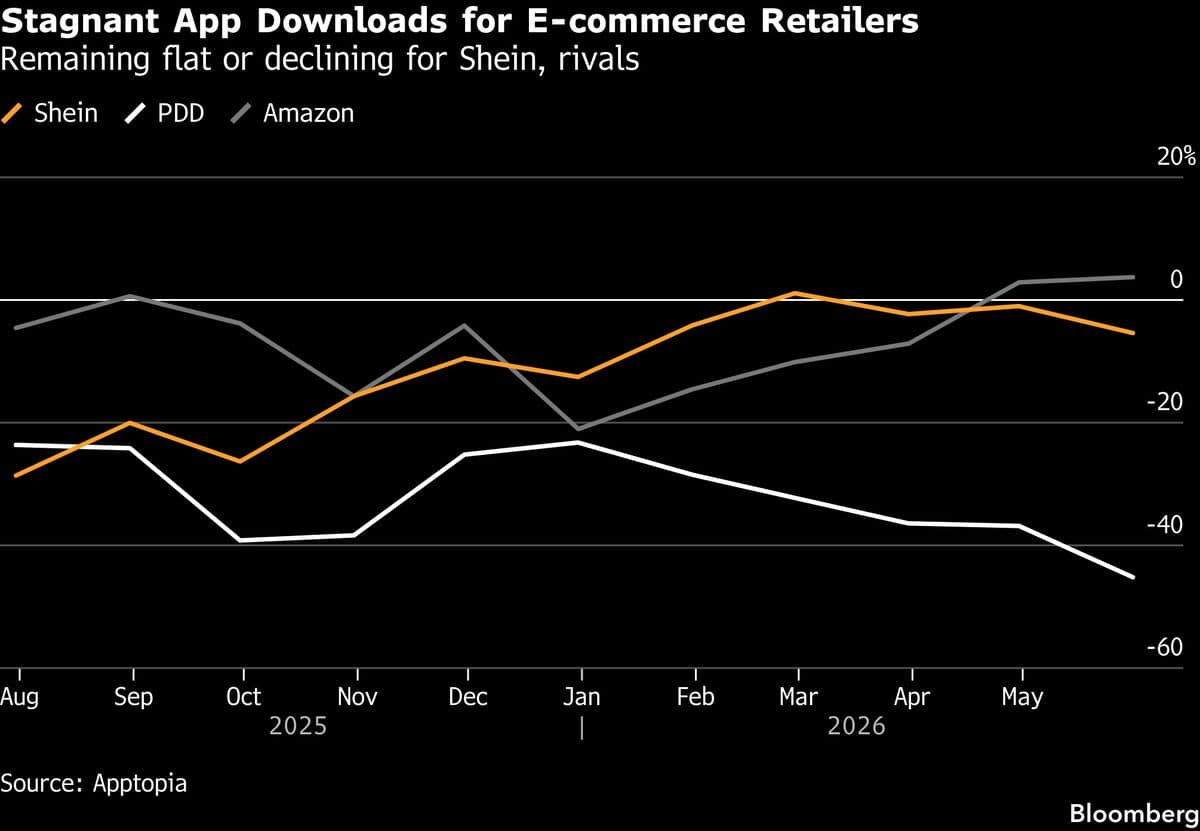

Shein has finally secured long-awaited Chinese regulatory approval for its planned Hong Kong listing, but slowing business growth threatens to weigh on the valuation it can command in the initial public offering. The fashion retailer's short-term growth targets, coupled with global demand contraction and supply chain adjustments, are beginning to strain investor risk tolerance.

Regulatory Approval and Valuation Impact

Asian Retail Market Dynamics

Markets view this as a critical juncture where Shein's credibility for worldwide growth may be tested. Low-margin expansion and rising supply chain costs are compressing the company's profit margins to 10% levels, potentially prompting investors to demand a higher risk premium on its shares.